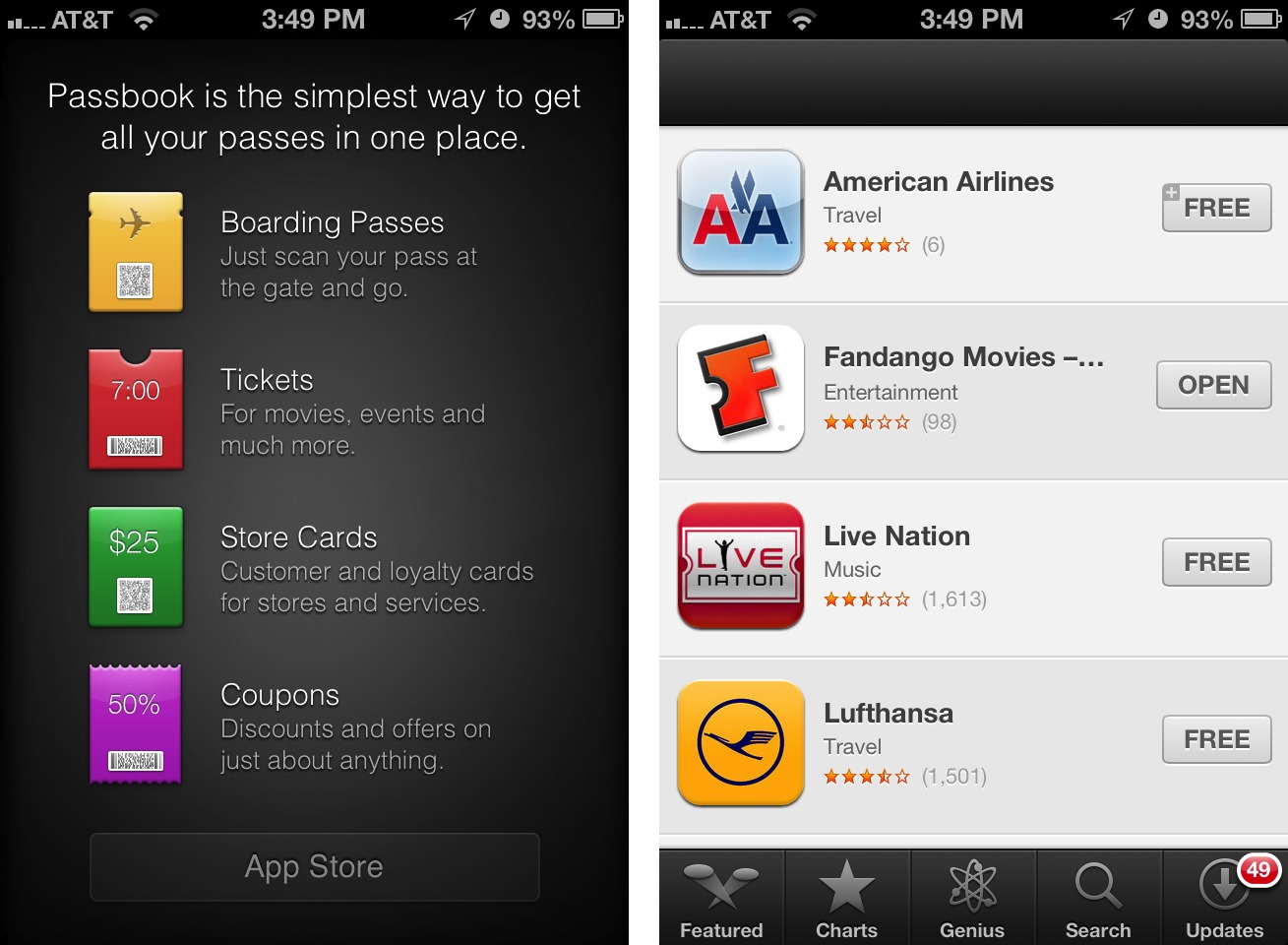

Passbook’s Best Is (Probably) Yet to Come

“The new Passbook app in iOS 6 — what’s that for, anyway?” I hear you ask. Apple may have demoed the potential for Passbook to manage coupons, boarding passes, tickets, affinity cards, and the other identifying paraphernalia of daily life among road warriors, but it seems mysteriously empty right now.

Passbook is simultaneously looking to the future while remaining firmly fixed in the past. Many transactions in our digital life that require a real-world component involve printing a sheet of paper that contains a barcode or a 2D tag (those areas of squares and rectangles that you can see at the very bottom right of this page — see “Tag, You’re in 2D!,” 1 October 2009) that’s scanned by a clerk or gate agent.

You might choose to turn such a document into a PDF or open it as HTML email on your smartphone, but not all scanners (still!) read smartphone screens, or the display scale might not be the right match for what the equipment can resolve. I often have to resort to punching in a long sequence of digits. In February 2012, at Pennsylvania Station in New York, I had to wait in a 20-minute line because Amtrak’s “bar-code scanners” wouldn’t recognize my phone’s screen, the number I typed in from it, nor the credit card against which I’d charged the ticket. (Amtrak, whose budget woes are deserving of pity, has upgraded its systems since).

I have many times expressed my love for QR Codes, the most popular category of 2D tags, because they provide a sort of analog glue between two separate digital systems. With a QR Code, you snap a picture of an item in a newspaper, on a poster, in a train schedule, or even off a computer monitor, and your device turns it into text or a URL. In actual practice (outside Japan), this is a multi-step operation: launch a special app, wait for the camera sheet to appear, put the tag in its view, wait for it to resolve, and tap, then wait for Safari to launch. (If Apple built 2D scanning right into the Camera app, it would be a different matter. See “Apple Could Make QR Codes Work with a Simple

Tweak,” 2 July 2012.)

But Passbook turns that process on its head. As a phone user, you don’t have to scan anything. In most cases, you will need an iOS app, like that of Fandango or United Airlines (already updated for Passbook), and the app will offer to add an entry to Passbook when you purchase a ticket or request a boarding pass. (The need for apps is why there’s an App Store button on the main screen of the Passbook app when it’s empty; tapping it displays Passbook-enabled apps in the App Store app.) This process will also work on Web sites, as the Passbook format is straightforward and a company has already started offering to produce them for businesses as a plug-in service. In theory, you can also receive a Passbook entry via email, though we

haven’t seen that in practice yet.

Many people were disappointed that the iPhone 5 didn’t support NFC (Near Field Communication), a set of standards that enable mobile devices to communicate with one another when in close proximity, and whose marquee use is contactless transactions. But NFC doesn’t have significant penetration in U.S. retail outlets yet, while barcode scanners that work with 2D codes on smartphones and, thus, Passbook are far more common. NFC may yet come to the

iPhone, and if it did, Passbook could evolve to transmitting the necessary data via NFC rather than relying on barcode scanning.

(NFC might be ready to make more inroads in the rest of the world where so-called chip-and-PIN credit cards are in use. With these cards, a merchant has to make an electrical contact to the card, and a customer types in a PIN. Only if the PIN matches does the card release its information for a charge. Customers and merchants are already used to portable charge terminals and entering a PIN. However, European colleagues tell me that the chip-and-PIN switchover was recent and costly enough that merchants might resist NFC, as it has no particular advantage in ease or cost savings.)

Over time, we’ll see Passbook entries for all sorts of things. Place an online order at a store with a brick-and-mortar retail shop, and the Passbook entry has the code to scan to pick it up. Or perhaps you’re browsing a Web site about coffee, and see a Starbucks ad offering a free latte; tap it, and the coupon is added to Passbook. Join an affinity program, such as a hotel’s loyalty program, and the card entry winds up in Passbook so you don’t have to carry an extra card in your wallet. I hope my local library, which has its own app that can show my barcode, adds my card’s info into Passbook as well.

The point of Passbook is to give you a single location to find all of these scannable documents, no matter where they’re generated. At some point in the future, there will be no more managing pieces of paper, PDFs, email messages, and separate apps for these bits of digitally displayed analog glue.

The other element of Passbook that we’ll be able to see only once it has really ramped up is location-based awareness. When you arrive at the airport for your United flight, Passbook will automatically bring up the boarding pass you need. Walk into a Starbucks store, and Passbook notifies you of a 20-percent-off coupon for the new triple caramel-encrusted macchiavelliano (if that’s not a Starbucks drink, it should be — the coffee whose ends justify the beans!). Digitally savvy muggers will be able to accost you in an alleyway, and Passbook will promptly give them a code to scan to empty your wallet. Perhaps that’s too speculative.

After a decade of mostly staying put in Seattle, I’ve started traveling again in the last year. I’ve been amazed at how the amount of user information I have to manage in some form has truly multiplied. On a single trip, I might need four boarding passes, a hotel affinity card, a car-rental affinity card, and a Starbucks card. Yes, yes, it’s a rough life, I know. But you may have seen the same clutter in your own life. Rather than stuff your wallet full of those cards and passes, why not have an app that does it for you?

At least, that’s Apple’s intention with Passbook. We’ll have to see how it plays out. Reports say Apple has major airlines, hotel chains, and retailers signed up. Any Web site or app maker should be able to play along easily as well, although it remains to be seen what sort of oversight Apple will apply and if Passbook will be truly open. The more the merrier — just as long as Passbook doesn’t become so crammed that I can’t sort through it, either.

One last note: If, like me, when you launch Passbook and tap the App Store link at the bottom of the main screen, an error appears that says “Cannot connect to iTunes Store,” there’s a trick to fix this bug. TUAW has the details, which involve setting your clock a year ahead and then back.

Has anyone associated with Tidbits compared Passbook to the Key Ring app? It deals with any 'wallet cards' with UPC codes.

I'm surprised it's not available on the iPad; I'd like Passbook there. But then, I'm amazed they finally added a Clock app....

I'm not completely surprised: although the iPad is a mobile device, it's much less apt to be in your pocket when you pop into your local Walgreens or movie palace. And, I imagine, it would likely be harder to scan as well.

Yeah, I'm thinking more about when traveling, plus my eyes aren't what they used to be, so I prefer the larger screen. It seems like it should be as easy to scan as anything else, or perhaps easier (CVS, movie theaters, Giant self-checkout, some airlines at the gate, et al. use hand scanners).

Plus I know a few people who do take their iPads *everywhere*.

Regardless, it seems pointlessly limiting. Like Clock, there's no technical reason to restrict it to iPhone or (I presume) iPod Touch. Perhaps, like Clock, it'll show up on the iPad in several years. ;-)

Whoops, sorry, I meant that Giant uses a flat self-checkout scan that is as easy to put an iPad on as an iPhone. They don't use hand scanners. My brain took a brief vacation there, sorry.

Re triple caramel-encrusted macchiavelliano: don't you mean the ends justify the beans?

I'm going to program a way to feature comments just to be able to push your comments to the top.

Find me at Macworld Expo some time and I'll buy you the closest thing to a triple caramel-encrusted macchiavelliano that Starbucks makes. :-)

Passbook's got great potential, in terms of new marketing possibilities for companies and also for final users, who can finally have a complete and updated wallet on their smartphones. Geolocalization and real time updates of your passes (whatever they are - boarding passes or concert tickets) are just two of the features that will completely change companies' marketing approach to their customers. It goes without saying that great companies are implementing this system. I've read about Sephora, Starbucks, Lufthansa and others, interested in Passbook adoption. And it will be booming.

There are many web applications that allow pass creation and help you better understand Passbook feature and potential. Developers are working hard to provide business and users a simple and quick way to implement Passbook app in their plans. I think one of the web app, between the many, is passdock.com, which is very simple to use but has got every feature you need to manage passbook passes.

We've had NFC here on Mallorca, Spain for quite some time already and it works seamlessly.

Also, Chip&Pin has been around for ages and, in the UK, for at least fifteen years, for God's sake. Neither was it costly to set up. Even the smallest of banks and retailers are on board.

The history in the UK dates to a roll out in 2004 and 2005, and it wasn't mandatory until about 2007. Perhaps that's not "recent" by a good measure. And the requirement for all merchants who accept credit cards (by issuing banks and networks) to upgrade equipment isn't the same as it being cheap. Everyone had to do it, and there was little to no benefit to the merchant except a potential reduction in chargeback fees as an opportunity cost (that is, cards that, in the old system, they would have accepted and then had to accept the loss).

From what I have been told and read, NFC will carry costs because new kit is required. Merchants that lease terminals, especially independent hand-held ones that talk right to bank systems, would just need to swap these out. But the lease for upgraded systems could be higher. Those that own terminals or have integrated point-of-sale systems will have to replace readers at every location and possibly upgrade back-end software, and so forth. Not necessarily cheap, but part of doing business.