How to Use Apple Pay

iOS 8.1 brought Apple Pay to Apple’s most recent iPhone and iPad models (see “OS X 10.10 Yosemite, iOS 8.1, and Apple Pay Have Arrived,” 20 October 2014), but unless you were waiting for the feature, you weren’t even given a clue that it’s now a thing, much less how to use it.

For those not in the know, Apple Pay is Apple’s new payment service, which lets you securely store credit card information to make purchases using the iPhone 6, iPhone 6 Plus, iPad Air 2, and iPad mini 3 (for more, see “Apple Pay Aims to Disrupt Payment Industry,” 9 September 2014). The iPhone 6 and 6 Plus allow in-store and online purchases, while the new iPads support only online purchases (see “iPad Air 2 and iPad mini 3 Expand the Line,” 16 October 2014).

In the physical world, Apple Pay relies on a technology called near-field communication (NFC). To use it in a store, a few conditions have to be true:

- You must have an iPhone 6 or 6 Plus with iOS 8.1 or later.

- The merchant must have an NFC reader.

- The merchant must have a relationship with Apple. (Or at least we thought that was true before the news about Rite Aid and CVS broke; now we’re less sure — see “The Real Reason Some Merchants Are Blocking Apple Pay… for Now,” 26 October 2014.)

But first, you have to set up Apple Pay.

Setting Up Apple Pay — To use Apple Pay, you must have a credit or debit card whose issuer has signed up to support Apple Pay. Whether your card will work with Apple Pay is a bit of a guessing game. For example, the Amazon Chase Visa didn’t work with Apple Pay at first, but it now does. Apple has a short list of participating banks, but it doesn’t help much. This Apple support document is more specific, but still confusing.

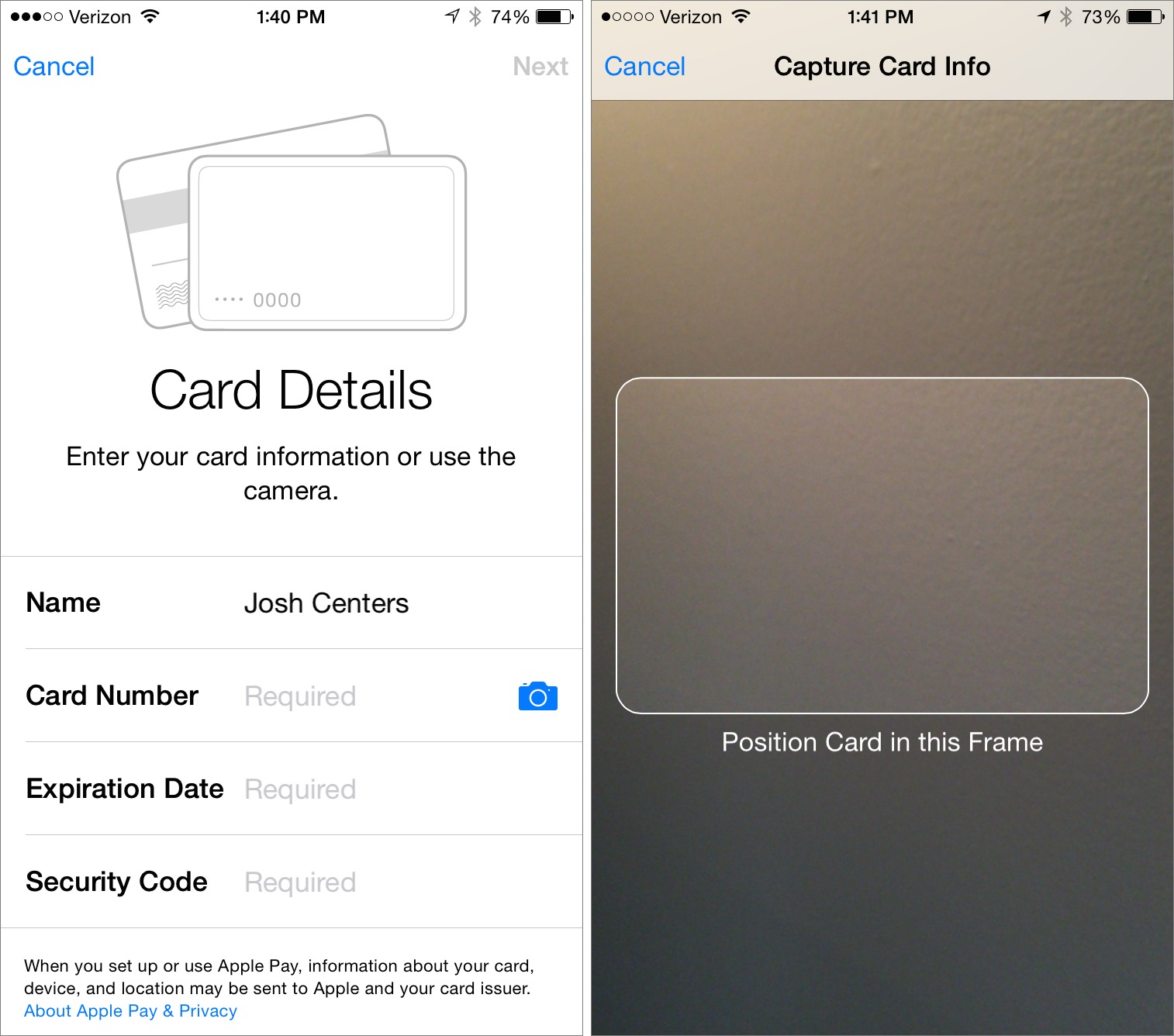

To manage Apple Pay, you use the Passbook app, which you may never have opened before. Tap the plus button in the upper right, or if you don’t see it, drag the visible cards down until you do.

Under Credit and Debit Cards, tap Set Up Apple Pay, and enter your Apple ID password if prompted. You now have two options: Use Card on File with iTunes (easiest) or Use a Different Credit or Debit Card.

If you choose to use a card already on file, you merely need to enter the security code from the back of the card and tap Next. Agree to the Terms and Conditions (twice), and then select a verification method.

If you want to add a card other than what’s on file with iTunes, you can either enter the information manually (boring) or tap the camera icon to scan your credit card’s information with the camera (cool). Make sure there’s plenty of light in the room and position your card so that it fits in the on-screen frame. When recognized, the card should be added automatically, but you must still add the security code manually.

After adding your card, you need to verify it with a secondary code from your bank. How the verification proceeds depends upon your bank, but in the case of Chase, they wanted to provide me with a verification code via email, a text message, or a phone call. I first tried email, but Passbook told me the code was expired. I tried again with a text message and it worked fine. So if one method doesn’t work, try another.

Back at the main Passbook screen, you’re prompted to tap Enter Code and input your verification code. If you want to change methods, tap Select a Different Verification Option.

Once you have received and entered your verification code (or have called your bank to verify), you should be good to go.

I tried three cards: a Chase Visa, an Ally MasterCard, and a MasterCard from a regional bank. Only the Chase Visa was accepted. Unfortunately, despite Apple working out deals with the major credit card networks, each institution must sign up individually, so if you use a small bank or credit union, expect a long wait before you can use Apple Pay. Even some cards that seem like they should be supported, such as the Citi-managed AT&T Universal Card that TidBITS publisher Adam Engst has, aren’t.

Using Apple Pay in the Real World — If you’re lucky enough to have a compatible card, it’s time to hit the town!

But where can you use Apple Pay? Again, the Apple Pay Web site has a list of partners, but that’s not convenient to reference when you’re out and about.

Apple also says to look for one of two icons: one that looks like a sideways Wi-Fi icon with a hand, and another that specifies Apple Pay. But the first icon merely indicates that the point-of-sale (POS) terminal is NFC-compatible, and isn’t a reliable indicator that you can use Apple Pay. Apple Pay requires NFC, but the NFC payment infrastructure can handle services other than Apple Pay as well.

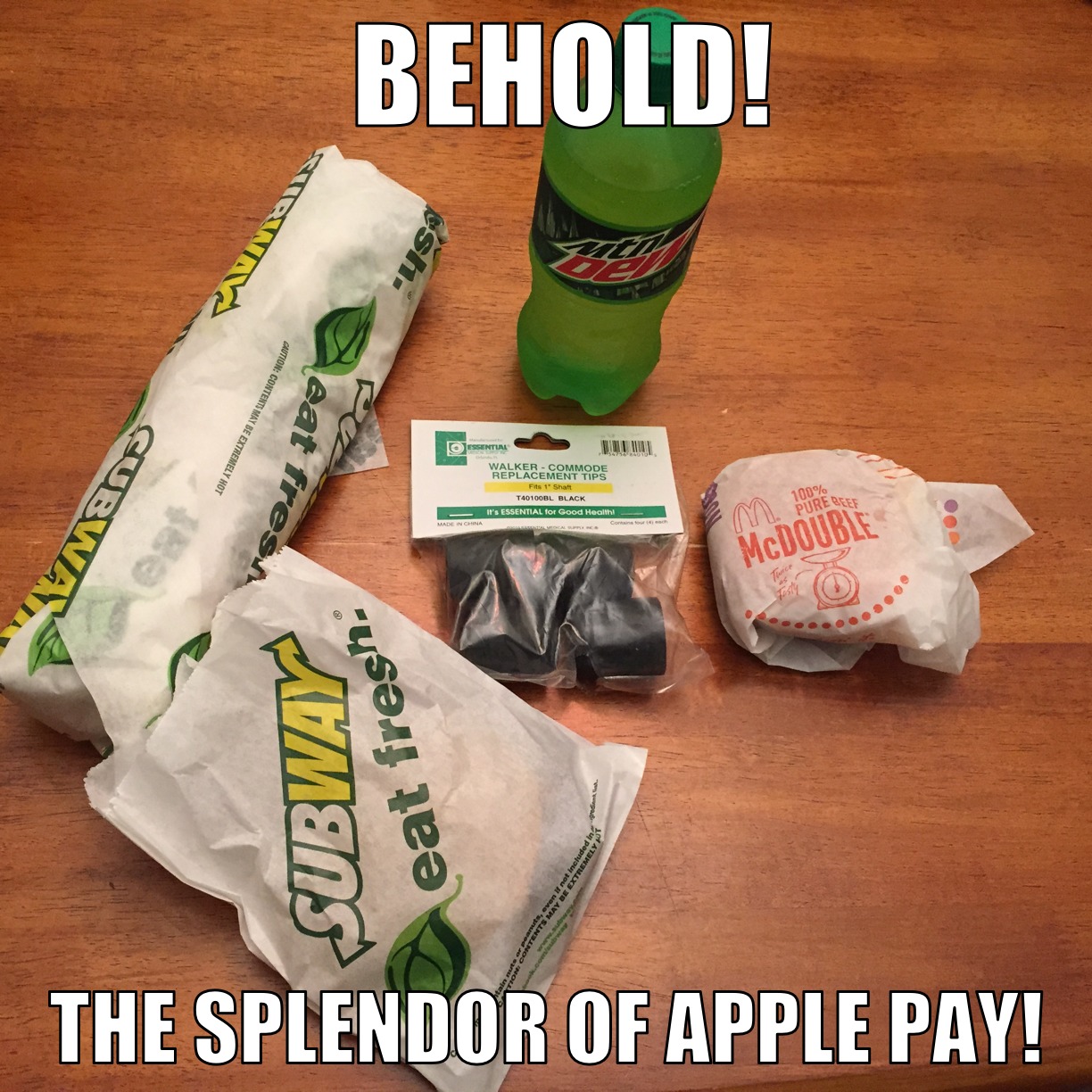

To test Apple Pay, I visited a few locations in my small town that I knew either had NFC-compatible POS terminals or were Apple Pay launch partners:

- Speedway gas station

- Walgreens

- Subway

- McDonald’s

My first stop was the Speedway around the corner. Despite it not being listed as an Apple Pay partner, it had NFC-compatible POS terminals installed recently, so I was curious if Apple Pay would work.

First, a brief explainer of how you actually use Apple Pay when checking out. It’s dead simple: hold your iPhone up to the terminal, which automatically wakes up the phone. If you have more than one card registered, tap it on the iPhone’s screen, and then place your finger on the Touch ID sensor. You can also opt to enter a passcode instead. Plus, if you place your finger over the Touch ID sensor before scanning, it automatically uses the top card in Passbook.

After your fingerprint is scanned (or you enter a passcode), Apple Pay goes through an authentication routine. If all goes as planned, the payment processes and you receive a notification on your phone displaying the payment location and amount.

Alas, that’s not what happened the first time I tried Apple Pay. The charge was declined, just as though I were over my spending limit. I wasn’t expecting it to work, since Speedway is not an Apple Pay partner, but I was a bit frustrated by the lack of a detailed explanation. I quickly explained myself to the confused clerk, paid with my debit card, and moved on.

The next stop was Walgreens, a chain I’m fond of because it’s always on top of the latest tech developments. It’s the only store where I frequently use Passbook (for my loyalty card) and it has had NFC-compatible POS terminals for years. Despite a warning from the cashier than an earlier attempt at Apple Pay failed, I successfully purchased a Mountain Dew and rubber walking-cane tips (I feel healthier already!).

It was long past dinner time, so next I rolled into Subway, another Apple Pay launch partner. When it came time to check out, I was confused, as there was no NFC symbol on the credit card reader. I warned the cashier in advance and gingerly placed my iPhone 6 to the reader. Surprise, it worked, and I left with my steak and bacon sub and cookies (I’ll be Jared-fit in no time!).

Finally, I visited McDonald’s, arguably Apple Pay’s flagship partner. The company even developed a wacky drive-through POS system for Apple Pay. I wasn’t feeling brave enough to try the drive-through, so I walked in. The purchase of a McDouble (I had missed lunch!) went smoothly, and the cashier actually knew what was happening.

After several purchases with Apple Pay, I can say that the process feels magical — when it works. But one problem, at least for now, is that most of what I can buy with Apple Pay is garbage.

You may be curious what the receipts show, since one of the key advantages of Apple Pay is privacy. Apple claims that the cashier won’t know your name or see your card number. My receipts from Walgreens and Subway appear just as if I had used my credit card, showing that I used a Visa, along with the last four digits of the device number. The McDonald’s receipt shows the same and also indicates that it was a contact-less payment. However, none of the receipts show my name, which is a privacy plus.

Using Apple Pay Online — An overlooked aspect of Apple Pay is that it can be used to pay for physical goods and services within iOS apps (but not via the Web). Some apps that support Apple Pay are: Apple Store, Target, Uber, OpenTable, and Groupon. Unlike physical payments, you can use in-app Apple Pay with the new iPad Air 2 and iPad mini 3, both of which have Touch ID.

I think this aspect of Apple Pay has been woefully downplayed. For kicks and giggles, I downloaded the Target app and bought some paper towels. The entire process took, at most, two minutes, and didn’t require me to set up an account. It was the most frictionless online purchase I’ve ever made (factoring in account setup time).

It’s as simple as tapping the Apple Pay option when it’s time to pay, then placing your finger on the Touch ID sensor. Apple Pay fills in your shipping details, and you’re done.

Online retailers who provide iOS apps would be stupid to not get on board with Apple Pay. Setting up new accounts is my biggest barrier to entry, and one reason why I shop at Amazon so frequently. But Apple Pay makes it just as easy to buy from any other retailer. If Amazon doesn’t want to be left behind, it had better get on board, too.

Managing Apple Pay — As I mentioned above, you receive a notification whenever an Apple Pay payment is processed. You can view these in Notification Center.

To see more information, open Passbook and select your card. It lists your most recent transactions.

![]()

Tap the info button for additional settings. If your financial institution has an iOS app, it will be linked to here. Other settings enable you to disable notifications, contact your institution, and remove the card.

The Verdict on Apple Pay — My early impressions of Apple Pay are positive. Like any good Apple innovation, it feels magical when it works, and it promises a solution to what seems to be a never-ending stream of credit card number thefts (the most recent being Staples, which has signed on with Apple Pay). But like any fledgling technology, it has challenges that must be overcome.

The first, and most obvious, challenge is participation by both financial institutions and retailers. For me to pull out my iPhone instead of my debit card, I need to know that Apple Pay is going to work every time, and that demands ubiquity. Unfortunately, I don’t see that happening in the near future. Two of the largest U.S. retailers, Walmart and Best Buy, are flat-out rejecting Apple Pay for a competing system that doesn’t require NFC. Best Buy has tried NFC in the past, but said it was too expensive to maintain.

The other end of that equation, financial institutions, doesn’t look much more promising. Sure, the banks are enthusiastic about Apple Pay as a way to prevent fraud, but if each has to sign an individual agreement with Apple, it could take years before they’re all on board. I’m hoping Apple can work out some arrangement with the credit card networks to speed up adoption.

The second, equally crucial challenge is education. After installing iOS 8.1, I had no idea how to set it up. Unlike setting up Touch ID when I got my new iPhone 6, there were no prompts to set up Apple Pay. I found it in Passbook by sheer guesswork, but how many normal users would think to do that? Who even opens Passbook enough to remember it’s there?

And once it’s set up, there’s no clues about how or where to use it. I had seen Apple’s original announcement, so I knew it involved touching the phone to… something. But what do you touch it to? The credit card scanner? The register? Do I hand my phone to the clerk? How do I know it’s compatible? I have yet to see a sign or banner that says, “Apple Pay accepted here!” If I were a normal person who doesn’t stay on top of tech news, I’d have no idea how to use Apple Pay.

It’s not just the customer who’s confused: the cashiers seem equally uninformed. The cashier at Subway acted as though I were a wizard. And I don’t blame her! If I had been in her shoes, I would probably have been a bit flabbergasted as well. Cashiers at Walgreens and McDonalds seemed equally awestruck, even though they at least understood what I was doing. (As a side note, I’m waiting for a clueless manager somewhere to think an Apple Pay customer is “hacking” the register and call the police.)

If Apple is serious about Apple Pay taking off, it’s going to have to help businesses educate customers and employees. Employees should know what Apple Pay is and know how to help customers use it. Customers shouldn’t have to guess if they can use Apple Pay or not. There should be clear signage, both on the door of the business and at the POS terminal, with brief instructions.

My prediction is that Apple Pay will be a success, but not in the way most analysts have imagined. The focus has mostly been on the in-store aspect, but I think that end will take years to achieve widespread adoption, because not every retailer will want to shell out for NFC readers, and if Apple Pay isn’t ubiquitous, users will forget about it as soon as the novelty wears off, unless they have additional incentive to use it. (There is already talk of integrating Apple Pay with loyalty programs, which would at least guarantee that I’d use it at Walgreens.)

Where I do think Apple Pay will succeed is with apps. One of Amazon’s biggest advantages in the retail space is that just about every online shopper has an account and associated payment method. If I have the choice between buying an item from Amazon or a competitor, I almost always choose Amazon because it’s more convenient.

Apple Pay removes that friction entirely, putting every online retailer who participates in Apple Pay on equal footing with Amazon (potentially better footing, since Apple has more credit card numbers on file than Amazon).

There are two potential snags in Apple Pay’s online dominance. The first is that it works only through iOS apps, and not on standard Web sites, which is limiting. The greater snag is that Apple Pay requires the latest iOS hardware: an iPhone 6, iPhone 6 Plus, iPad Air 2, or an iPad mini 3. Great as these devices are (well, except for the utterly boring iPad mini 3), even loyal Apple customers won’t necessarily upgrade their existing devices for another year or two.

The reason for this hardware requirement is that Apple Pay stores your credit card information not in flash storage or (heaven forbid!) iCloud, but in the A8 and A8X processors’ Secure Element. The A7 featured a Secure Enclave to store fingerprint data, but it presumably is incapable of storing credit card data.

While it’s good that Apple is taking security with the utmost seriousness, I fear that this limited device compatibility will hobble Apple Pay out of the gate. Or, perhaps that’s why Apple isn’t saying much about it now — perhaps the big push will come in another year or two once the bulk of iOS devices support Apple Pay.

Think about that. Maybe, just maybe, these snags have been left in intentionally. Apple has a chicken-and-egg-and-frying-pan problem: it needs to lure banks, retailers, and users while also keeping things manageable.

Apple is notoriously bad at the things it doesn’t excel at. Take cloud services. The company has struggled with them for nearly fifteen years between iTools, .Mac, MobileMe, and iCloud.

But people are willing to put up with problems with online services. We may squawk, but we’re not that perturbed by servers going down, spotty connections, and other things that go bump in the net. When Facebook founder Mark Zuckerberg declared, “Move fast and break things,” he encapsulated the cloud development philosophy perfectly.

With Apple Pay, though, Apple is offering a financial product, which is different from anything the company has created so far. I know, I used to work in finance, where the philosophy is: “move slow and don’t touch anything!” The world of finance is tightly regulated. One mistake could cost Apple a lot of money, or even worse, land someone in jail. And while users might forgive and forget that email outage, they’ll break out the tar and feathers if Apple Pay loses track of their money.

Apple Pay has to scale up slowly, but there’s no such thing as a “beta” financial product. No one would use it. So what does Apple do instead? Make Apple Pay sort of difficult to figure out. That won’t slow down the small pool of early adopters who will breathe life into the system while Apple works out the kinks. But it will keep the masses in the dark.

Those early adopters will explain Apple Pay to their friends and family, and if Apple is lucky, Apple Pay will trickle down through the technical literacy ranks at a pace Apple can keep up with while learning the financial industry ropes.

In a year or two, once Apple has figured out the Apple Pay business, and how to scale it properly, then the company can unleash a wave of marketing and education to corner the market. With enough customers demanding Apple Pay, even the most stubborn retailers will have a hard time balking.

If Apple Pay works, it couldn’t be a better side business. Apple reportedly gets a 15-cent cut out of every $100 it processes. That doesn’t seem like much, but scaled up, it means a nice chunk of mostly passive income. Apple doesn’t have to design anything, build high-tech factories, buy raw materials, or do anything but track the virtual money we send through its servers.

Whether Apple Pay survives in the long run or fades into history, it’s still a neat system with a lot of promise, and is one of Apple’s coolest new initiatives in years. Here’s hoping it insinuates itself into our lives more than, say, iBeacon.

I have tried several times to use Apple Pay to purchase items using the Groupon app, and every single attempt has failed with a message in the app, "Order failed: One or more fields contains invalid data"

The Passbook shows the transactions with no indication of failure.

I have tried these transactions with a Chase Freedom credit card, a Chase debit card, and an American Express card. All three cards were successfully (apparently) entered into the Passbook, and I received confirmation emails from Chase and Amex.

I have not yet tried with any other app, or had an opportunity to try an in-store purchase.

Try going to Settings > Passbook & Apple Pay, and look under the heading "Transaction Defaults". Are *all* of the entries, such as Billing Address, Shipping Address, etc., filled in?

Unfortunately, these fields are unrelated to using Apple Pay in stores, so you aren't asked to fill them out if you simply add a card to passbook. However, all of these fields are required in order to use Apple Pay via an app, as you might imagine.

Rich, I was having the same exact issue with the Groupon app and Apple Pay. Through trial and error I determined the issue was that my billing address had a zip+4 format zip code. When I created a new shipping and billing address in the Passbook and Apple Pay settings with just a five digit zip code, all of my Groupon Apple Pay purchases now succeed. I've reached out to Groupon support and gave them the details of my issue. They're working on a fix for zip+4 now.

I didn't think to try Passbook. Instead I went into the Settings app, where I found a top level entry for Passbook & Apple Pay. It let me put in my first credit card (the same one on my iTunes account, not that it mattered), and then I headed over to my local Apple Store. Turns out they have a demo set up with their handheld scanners, so I was able to try out Apple Pay without having to buy anything. First time for the Apple employee too, but it all went without a hitch. Can't wait to buy something for real.

Regarding Adam's failure to get his AT&T Universal card (issued by Citibank) accepted:

I too have a that kink of card and was rejected. I followed up with Citibank's phone support and was told that it was declined because the card is close to expiring (it has a 12/14) date and that a new card with a new security code should be accepted.

Note that I was able to use the card for an online purchase (an update license for BBEdit) shortly after this interaction.

I'll have to call them when I get a chance. My cards are far from expiring (7/16) so it shouldn't be that alone. But perhaps there's some new security code that needs to be put in place.

When my attempts to validate my AT&T Universal Card on Apple Pay setup failed I called the 800 number on the back of the card. There was no prompt to talk to a human, but finally I tried 0 and it worked.

After talking with a few people, the representative came back on line and reported that AT&T Universal Card was not supporting Apple Pay at this time. My expiration date was not near expiring.

And that means I don't support AT&T Universal Card at this time. and Into a drawer it goes. I've got another VISA card I can use instead.

My iPad Mini 3 has a NXP Semiconductors 65V10 NFC Controller chip in it according to the iFixit teardown. That is the same NFC chip that is in my iPhone 6, so why won't Pay on the Mini 3 work just like on the iPhone 6? If iPads are NOT to be used for Pay via NFC, then why do they have the chip installed?

That's an interesting question. The short answer as to why Apple Pay won't work in stores is that the iPad mini 3 doesn't have the necessary antenna. The theory I've heard about why the NFC chip is there is that's where the Secure Element, where all of your payment info is stored, resides. However, that contradicts Apple saying that the Secure Element is in the A8.

"...things that go bump in the net"

I came over from my email TidBits, and bothered to log in, just so I could say this: Well done, sir.

Thank you! It's a classic phrase that must be dusted off every so often for a new generation. :-)

Are you guys going to do a piece on how I as a small business can set up Apple Pay to offer to my clients? I myself want to integrate into our self-serve kiosks but I am sure there are plenty of stores with Mac-based Point-of-sale.

Can I use any NFC device?

Any known solutions for integrating with our Filemaker Pro solution?

An interesting question - at the moment, I can't find a single piece of information about this. Clearly, it must be associated with getting an NFC-compatible POS terminal, but beyond that, I just don't know. We'll keep looking...

FYI, the list of financial institutions that are going to add apple pay is quite long. They aren't live yet as they need to update their backend to deal with tokenization, but they include my credit union and favorite bank.

Here is the list:

http://usa.visa.com/clients-partners/technology-and-innovation/apple-pay/financial-institutions/index.jsp

I have a question. My husband and I own a business and just updated our terminals to accept apple pay. The problem I have is that we don't use a cash register that automatically sends the amount to the terminal. How would someone go about using apple pay at our store if there is no amount sent to the terminal? Can the customer place their phone by the screen and then select their card and specify an amount?

Hmm, that is a good question, and I'm afraid I'm stumped. I would suggest trying it out or contacting your vendor. How do you handle credit card transactions? Does the customer have to manually input the amount?

We input the amount on the terminal then they select whether they prefer credit or debit, pin numbers, etc. The vendor knew everything about the machine except this. LOL. Apparently it is new to them as well...

Maybe just enter the transaction as if were cardless? But then I would still need the cards number and that seems more difficult than just swiping. Hmmmm. I too am stumped!