iPhone 14 Pro and Apple Watch Ultra Ordering Observations

I was so focused on writing about the new iPhone 14 and Apple Watch models for TidBITS and our TidBITS Content Network subscribers that I haven’t had much time to figure out what I wanted to do concerning upgrades from my current iPhone 13 Pro and Apple Watch Series 5. If a friend whose job didn’t revolve around covering Apple products had asked my advice, I’d recommend sitting tight. On the other hand, I benefit from having access to the latest and greatest Apple gear, and it can be helpful for coverage to get it as soon as possible—September 16th for the iPhone 14 and September 23rd for the Apple Watch Ultra.

After some pondering, I decided to upgrade to the iPhone 14 Pro so I’ll be able to evaluate the Always-On display and the Dynamic Island, plus take advantage of the improved cameras. I’m still on the fence about the Apple Watch Ultra. As a competitive runner, I’ve long criticized the Apple Watch’s physical design, and to this day, I usually strap a Garmin Forerunner 645 on my other wrist when I head out for a run, relying on the much-clumsier Apple Watch only when I forget the Garmin.

However, the Apple Watch Ultra promises to address my usability and screen readability complaints with its new Action button and a much brighter screen. Coupled with an app like WorkOutDoors, which sounds like it would enable an even more customizable interface than my Forerunner 645, an Apple Watch Ultra could eliminate my desire for a dedicated running watch. But $799 is a lot to pay to replace a functional Apple Watch Series 5 and the Garmin Forerunner 645 that cost me less than $300 (including the optional running dynamics pod) two years ago. Plus, the Apple Watch Ultra’s beefy size makes me want to try one on before buying, so I decided to hold off for now.

But getting to the point of making those decisions and ordering the iPhone 14 Pro wasn’t entirely smooth.

iPhone Upgrade Program Quirks

In the past, I’ve always purchased iPhones outright because Tonya and I would usually alternate years, handing the newest extra iPhone down to Tristan. Now that he’s buying his own iPhones and Tonya refuses to use anything larger than an iPhone SE, there’s no reason for me to hold onto my previous iPhone when upgrading. That made me think it was time to join the iPhone Upgrade Program, which splits the cost of an iPhone (plus AppleCare) over 24 months and lets you upgrade to the next model if you’ve paid at least 12 months, closing out the old loan and starting a new one.

However, after several trips through the purchase process, I failed to join the iPhone Upgrade Program. I ran into four obstacles along the way:

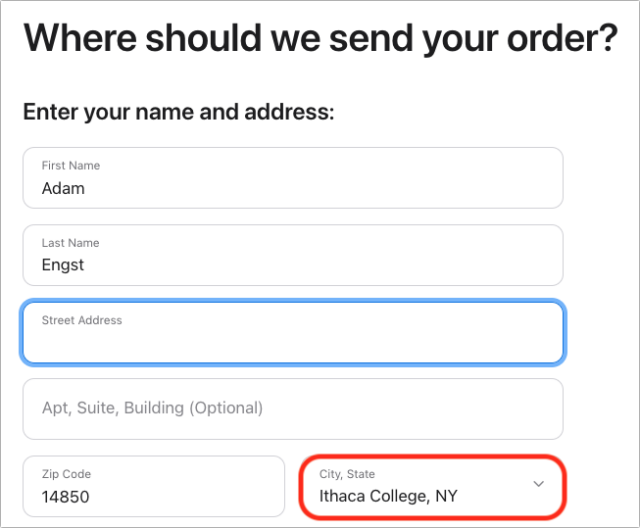

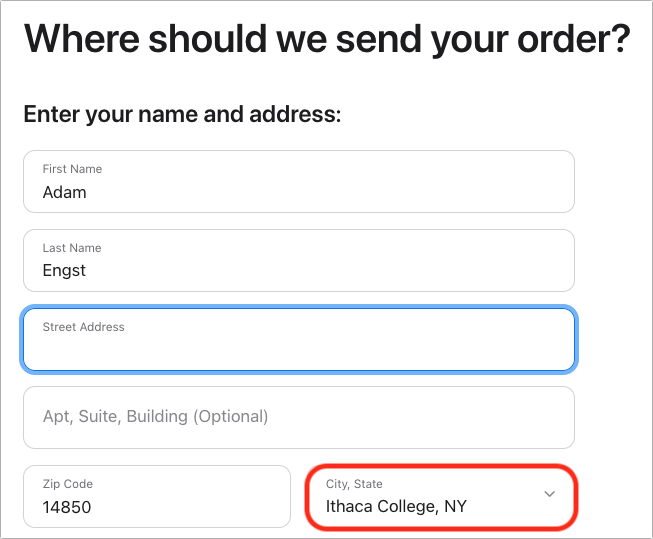

- Incorrect city lookup: I caught this error on Apple’s part on my second pass, and I’d encourage you to be careful. When I entered the ZIP code for Ithaca in Apple’s address form, it gave me a pop-up menu with three choices, defaulting to “Ithaca College” but also offering the abbreviation “Ithaca Clg” and the correct “Ithaca.” No other address form I’ve ever used had made that mistake (or even suggested Ithaca College), so I almost missed it. Who knows what that would have done to the eventual delivery?

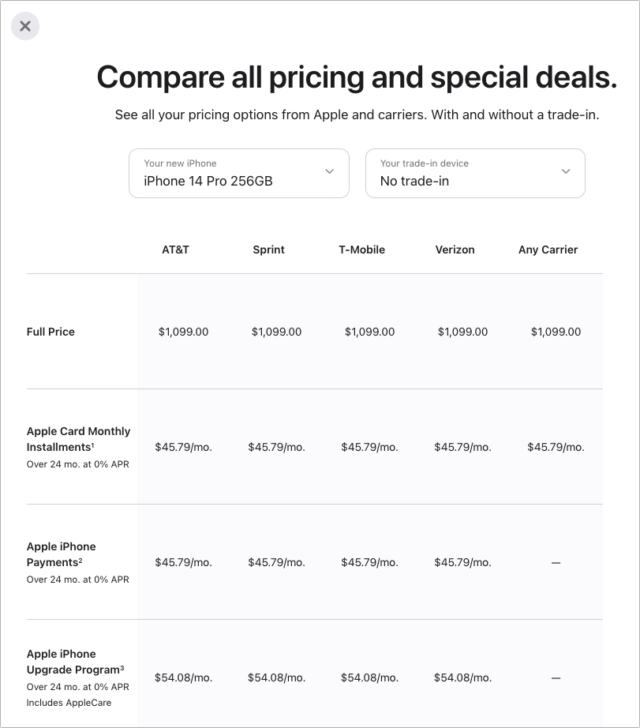

- Prices not reflecting trade-in: Apple provides a nice calculator that shows you how much you’ll pay for a new iPhone with or without a trade-in, using all the different approaches. The only problem is that when I chose the iPhone 13 Pro from the Your Trade-In Device menu, the iPhone Upgrade Program row disappeared. And indeed, when I got to the point of seeing a price for the iPhone Upgrade Program, it was $54.08 per month, which didn’t reflect the trade-in. I believe I could have just used the Apple Trade In program to trade in the iPhone 13 Pro separately for credit toward my next purchase or an Apple Gift Card, but it was still a confusing lapse in an otherwise well-designed process.

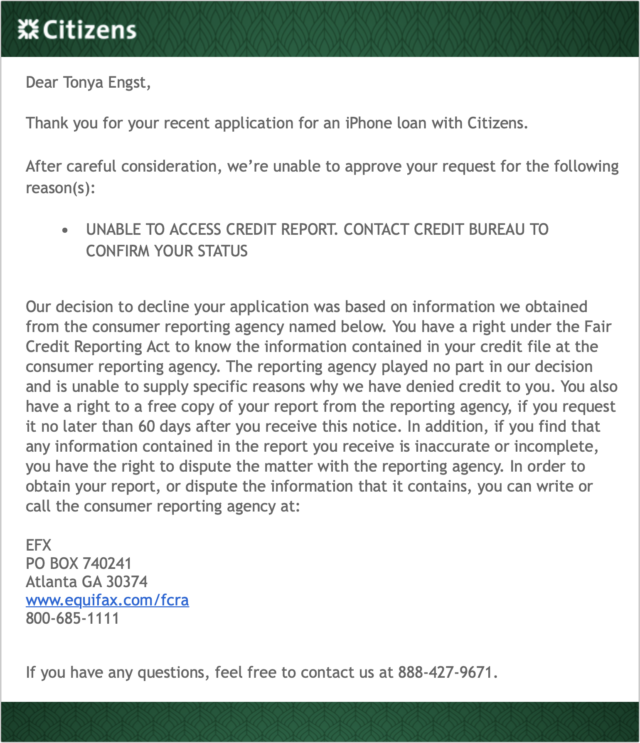

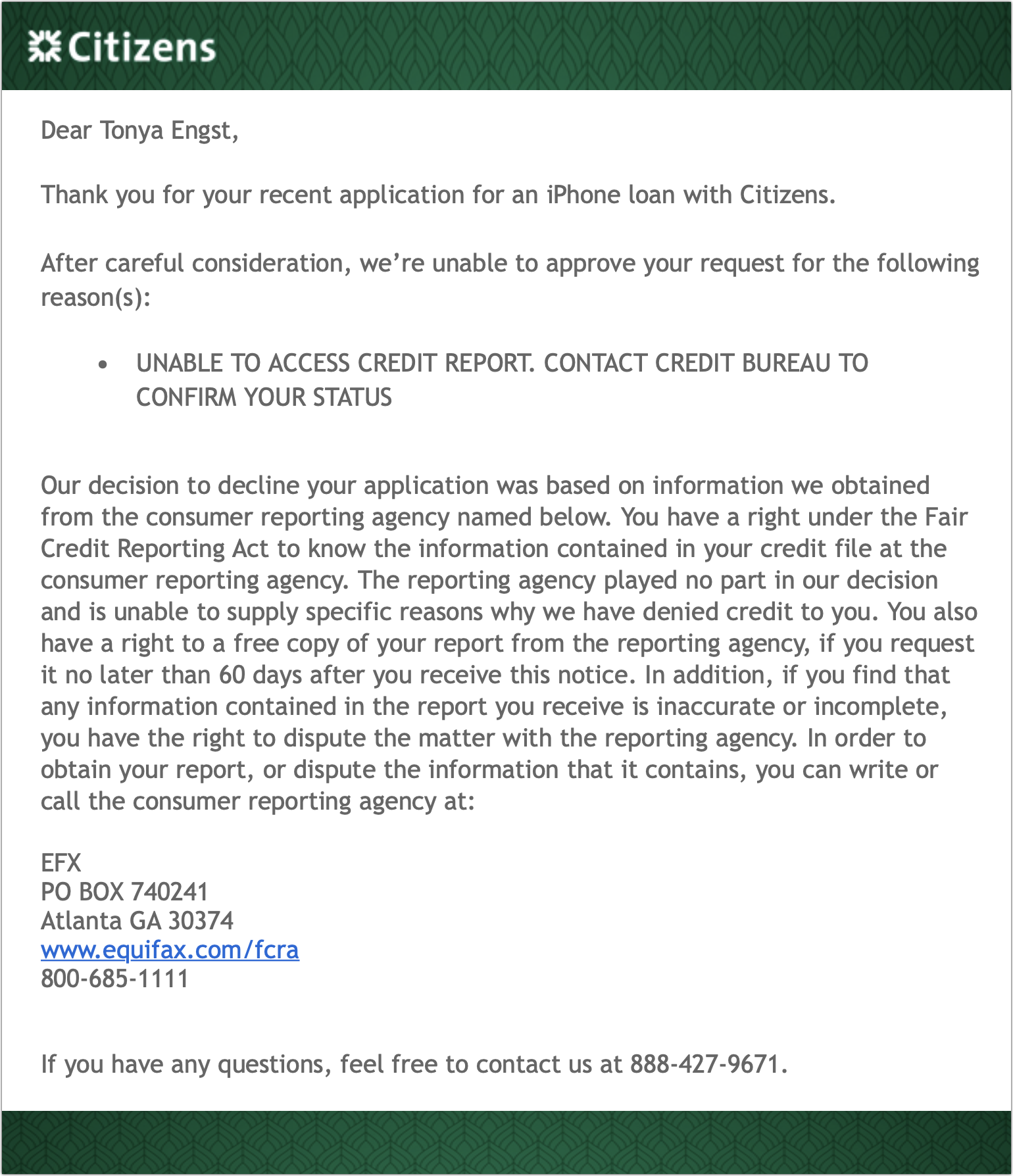

- Credit report frozen: We always keep our credit reports at Equifax, TransUnion, and Experian frozen to ensure that they can’t be used for identity theft. (And you should too!) However, because the iPhone Upgrade Program is essentially a loan with a 0% interest rate, Apple’s financing partner, Citizens One, needs to do a credit check. I didn’t think of that beforehand, so I was surprised to be rejected from the iPhone Upgrade Program on my first attempt. Apple’s website didn’t provide details about the rejection but said Citizens One would be in touch with the reason within 24 hours. I correctly guessed that the problem revolved around the credit report freeze, so I wasn’t surprised when Citizens One sent email 2 hours later confirming the problem.

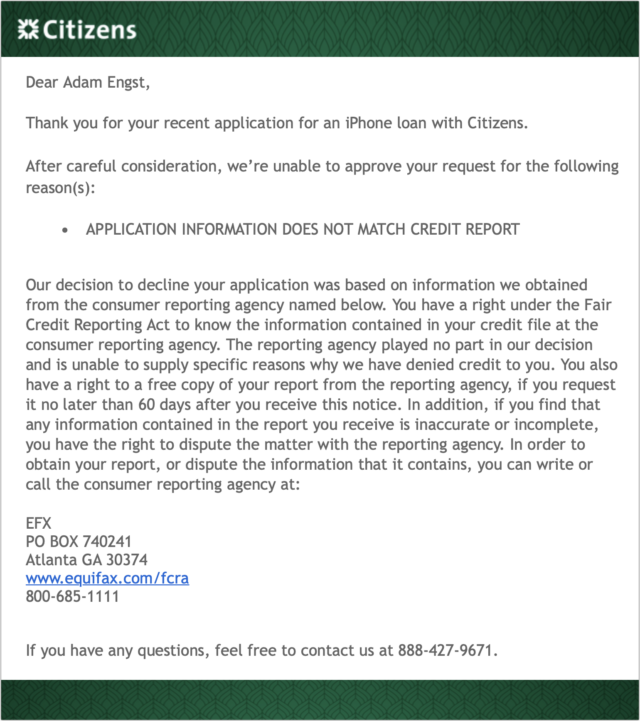

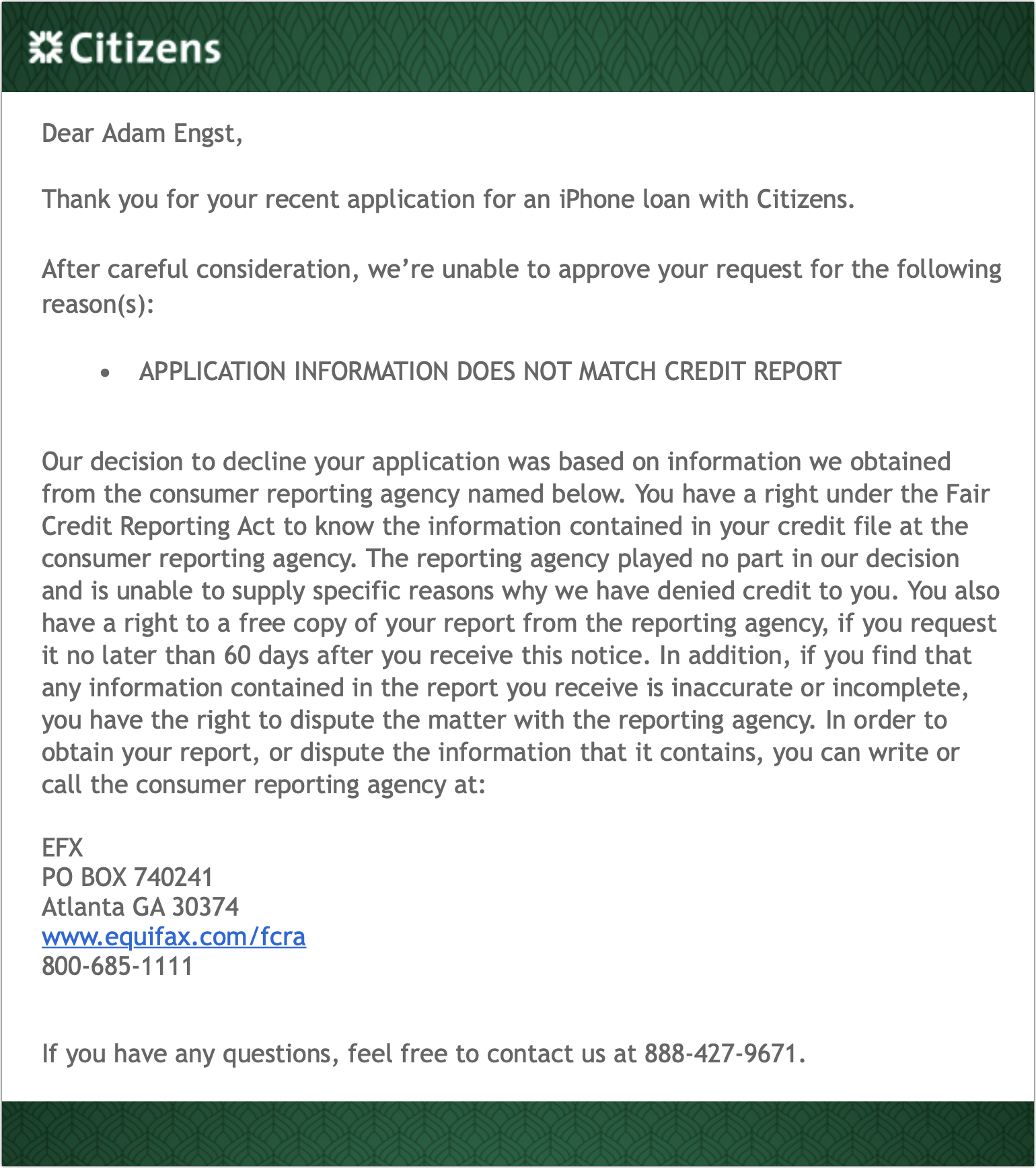

- Credit card name mismatch: Temporarily unfreezing (thawing?) both Tonya’s and my credit reports at Equifax resolved the previous problem, but my next pass through the iPhone Upgrade Program application failed again, generating a complaint about an information mismatch. I suspect the trigger may have been the fact that our business credit card is in Tonya’s name, but the purchase was in my name, which confused the link to the credit report. The email error that arrived 2 hours later didn’t help more, but note that this one uses my name rather than Tonya’s.

After the second rejection, I threw up my hands in frustration and decided to buy the iPhone 14 Pro outright and trade in my iPhone 13 Pro as part of that process.

Dealing with AppleCare During an Upgrade

Although I didn’t sit down with a spreadsheet to compare how the prices worked out with the myriad purchasing options, my quick estimates suggested that the result is nearly the same. Pay upfront for an iPhone, finance it over 24 months, use the iPhone Upgrade Program, whatever—you’ll pay the same amount.

Almost, that is. The main variable is AppleCare, which is optional for every approach other than the iPhone Upgrade Program. Take the AppleCare price—$199 for the iPhone 14 Pro—into account, and everything falls into line once again.

As I worked through the purchase, I realized that wasn’t quite true. I always recommend AppleCare for iPhone purchases, and I buy it myself. Previously, when I was keeping iPhones for 2 years, 2 years of AppleCare coverage matched perfectly. That’s what I bought with my iPhone 13 Pro last year. Since AppleCare goes with the device, trading in my iPhone 13 Pro would mean leaving a year of AppleCare coverage unused—roughly $100.

Luckily, it turns out that Apple offers pro-rated refunds of unused AppleCare coverage, saying:

If you cancel your AppleCare plan more than 30 days after your purchase, you’ll get a refund based on the percentage of unexpired AppleCare plan coverage, minus the value of any service already provided.

It looks like that requires contacting Apple support, so I’ve left myself a reminder to cancel after I return the iPhone 13 Pro to Apple. If you need to check your AppleCare status, look in Settings > General > About > AppleCare+.

For the iPhone 14 Pro, I decided to try the $9.99-per-month approach, though now that I’m not caught up in the rest of the purchasing decision, I realize that it will end up costing $20 more if I replace the iPhone 14 Pro next year or $40 more if I wait another year yet. Perhaps the capability to cancel an AppleCare subscription from the iPhone itself rather than calling Apple support will feel worth the difference. And, of course, if I decide to keep the iPhone 14 Pro for longer than 2 years, the monthly AppleCare+ plan might be welcome later on.

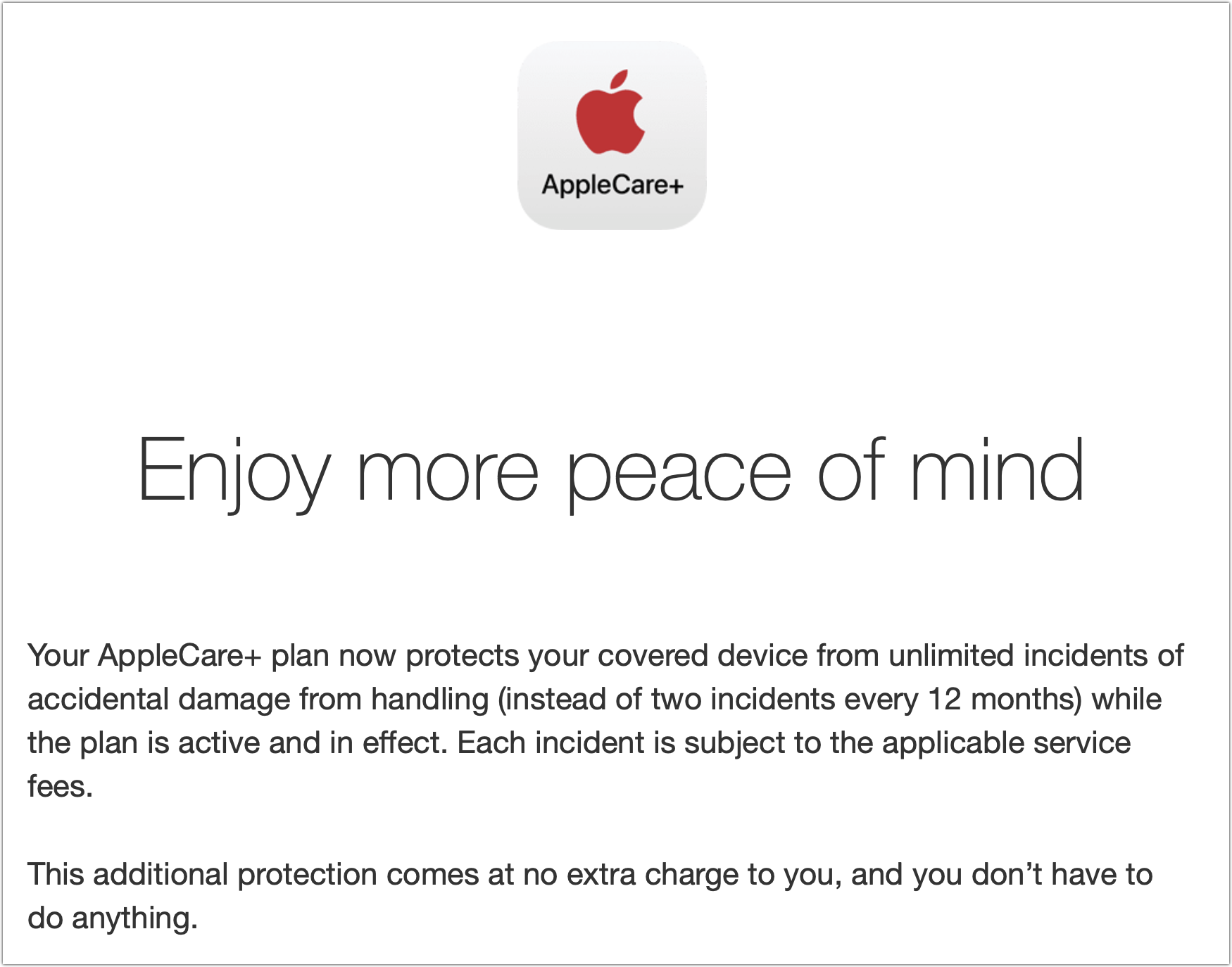

Two other AppleCare notes. First, Apple just improved the AppleCare+ coverage to include unlimited incidents of accidental damage protection. You’ll still have to pay something for each incident ($29 for screen or back glass damage, or $99 for other accidental damage), but you’re no longer limited to two incidents per year.

Second, Apple now offers another level called AppleCare+ with Theft and Loss, which costs $70 more than AppleCare+. It includes everything in AppleCare+, plus up to two incidents of theft or loss every year, with a $149 deductible. Paying $298 to replace a stolen $429 iPhone SE might not make sense, but shelling out $418 to recover from a loaded $1599 iPhone 14 Pro Max slipping out of your pocket in a cab feels more worthwhile.

Apple Watch Ultra Less Popular with Smaller People and Divers

Finally, while poring over the Apple Watch Ultra purchasing options, I noticed something interesting about the delivery dates. There are 18 possible configurations of the Apple Watch Ultra. The Alpine Loop comes in three colors and three sizes; the Trail Loop comes in three colors and two sizes; and the Ocean Band comes in three colors and one size. When I was writing this on 11 September 2022, there were four possible delivery dates:

- September 23: Small Green Alpine Loop, Yellow Ocean Band

- October 11–18: All other Alpine Loops and Ocean Bands

- October 25–November 1: S/M Black/Gray Trail Loop, Blue/Gray Trail Loop, Yellow/Beige Trail Loop

- November 1–8: M/L Black/Gray Trail Loop

I don’t know if Apple produced the same number of each of the bands or can produce more at the same rate. If those conditions were true, two bits of speculation would suggest themselves:

- On the unsupported assumption that people buy the Apple Watch Ultra band that goes with their sport, the later delivery dates could indicate that the Apple Watch Ultra is more popular with runners (Trail Loop) than adventurers (Alpine Loop) or divers and watersports aficionados (Ocean Band). Or perhaps there are just more runners. (The White Ocean Band was also promising earlier September 23rd delivery when I first looked two days ago.)

- People with smaller wrists, which would include more women, are less interested in the beefy Apple Watch Ultra, at least until they can try it on in person. Support for that comes from the Small Green Alpine Loop still being available for September 23rd delivery and the S/M Black/Gray Trail Loop being available sooner than the M/L Black/Gray Trail Loop.

Don’t read too much into that speculation—there are way too many unknowns—but it matches up with my overall opinions, so I’m going with it. And if my Apple Watch Series 5 gives up the ghost or starts to suffer from problematic battery life, I’ll see what Apple Watch Ultra Trail Loop combos are available then.

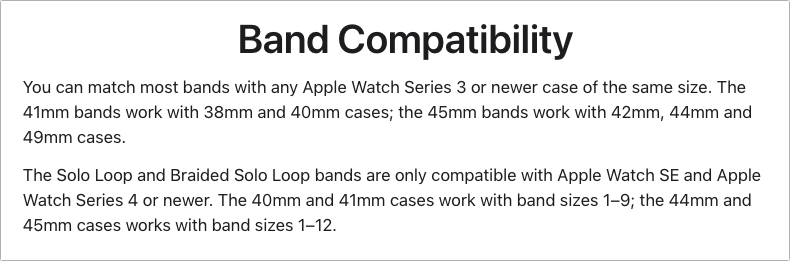

One final point. If you want to order an Apple Watch Ultra now and get it as soon as possible, buy whatever combination will arrive first and pair it with a different band, perhaps an inexpensive knock-off (see “In Praise of the Knock-Off Nylon Sport Loop,” 19 March 2021). Apple says that 45mm bands will work with the Apple Watch Ultra’s 49mm case, although it’s slightly unclear from Apple’s compatibility information if the Solo Loop and Braided Solo Loop will work. Similarly, the Apple Watch Ultra bands can be used with the 44m and 45mm Apple Watch case sizes.

They are. If you click the compatibility link in a solo loop or braided solo band page, the popup that shows up says this:

Right, but the next sentence in that pop-up, as shown in the article says:

If that last clause included 49mm in the list, I’d be certain. Realistically, it will probably work, but I don’t want to say that categorically without testing or Apple being crystal clear.

Would the larger size of the Watch Ultra mean that the same Solo Band that works on previous models would be too large for the Ultra? All other bands are adjustable and so can handle small changes, but a given solo loop size works only over a very narrow range.

Something to be aware of: your carrier may not yet support eSIM and thus not be compatible with the iPhone 14. I realized today that Consumer Cellular doesn’t support eSIM yet. Apple has a list of compatible carriers here:

According to that list, Consumer Cellular does support eSIM. That page lists three categories of support:

eSIM Carrier Activation. With this, your carrier can install/activate the eSIM at the time of purchase, or set it up remotely, so you don’t need to do anything special.

eSIM Quick Transfer. This allows you to transfer your activation from one eSIM phone to another without contacting your carrier.

Other eSIM activation methods. For example, scanning a carrier-provided QR code or using a carrier-specific app to install the eSIM.

Consumer Cellular is listed in the third category. The link Apple provides there is broken, so I don’t know any more details, but it is likely that if you ask them for eSIM activation, you will receive (probably via e-mail or directly from the web site) a QR code that you can scan with your phone to install the eSIM.